Behind the Scenes of Ecommerce Payments: A Beginner’s Guide

The Invisible Engine of Online Shopping

Ecommerce payment is the process that enables online businesses to securely accept and process electronic payments from customers. It’s the behind-the-scenes system that makes buying and selling online possible.

If you’re looking to understand ecommerce payments quickly:

| Key Aspect | What You Need to Know |

|---|---|

| Definition | Technology that securely processes online transactions between customers and merchants |

| Main Components | Payment gateway, payment processor, merchant account |

| How It Works | 1. Customer enters payment info 2. Gateway encrypts data 3. Processor authorizes payment 4. Gateway confirms transaction 5. Funds settle in merchant account |

| Common Methods | Credit/debit cards, digital wallets, buy-now-pay-later, bank transfers |

Processing payments might be the most nerve-wracking aspect of running an online store. After all, it’s where you seal the deal. If your payment system fails or frustrates customers, all your marketing efforts go to waste.

Consider this: studies show that 26% of customers will abandon their cart due to a complicated checkout process, and cart abandonment rates have been measured as high as 81% in some industries. That’s a lot of lost revenue simply because the final step in your sales funnel isn’t working properly.

But a smooth, secure payment process does more than just complete transactions — it builds trust with your customers and keeps them coming back. When shoppers know their payment information is safe and the checkout process is quick, they’re more likely to become repeat buyers.

Whether you’re just starting your ecommerce journey or looking to optimize your existing store, understanding how payments work “under the hood” is crucial for growth. The right payment solution can reduce cart abandonment, expand your market reach, and ultimately boost your bottom line.

Why Learn About Ecommerce Payments?

For beginners in the ecommerce space, payment processing might seem like a technical detail best left to the experts. But here’s the truth: understanding how your customers pay you is fundamental to your business success.

When you grasp the basics of ecommerce payment systems, you can:

- Make informed decisions about which payment solutions best fit your business model

- Troubleshoot issues that might be costing you sales

- Optimize your checkout experience to boost conversion rates

- Better understand your cash flow and settlement timing

- Implement stronger security measures to protect your business and customers

As one merchant told us after we helped optimize their payment system, “I never realized how much revenue I was leaving on the table with my clunky checkout process. Understanding payment flows helped me see the big picture.”

Understanding Ecommerce Payment Processing

Ever wonder what happens in those few seconds between clicking “Buy Now” and seeing your order confirmation? While it seems instant to shoppers, ecommerce payment processing is actually a carefully choreographed dance involving multiple financial partners and security checkpoints.

Think of payment processing as the invisible engine powering your online store. When a customer decides to purchase your handcrafted candles or custom t-shirts, here’s what unfolds behind the scenes:

First comes authorization, where your payment gateway forwards the customer’s card details to their issuing bank. The bank checks if sufficient funds exist and runs initial fraud screenings. Next, authentication might kick in through systems like 3D Secure, adding an extra layer of verification for the customer.

Within seconds, the issuing bank sends back an approval or decline. Upon approval, the transaction is captured for settlement, and your customer sees that satisfying “Thank you for your order!” message. Finally, settlement occurs when the funds actually move from the customer’s account through the acquiring bank and land in your merchant account—typically within 1-3 business days.

As one of our Nashville boutique owners shared: “Understanding the difference between authorization and settlement completely changed how I manage inventory. Now I know a ‘sale’ doesn’t mean money in the bank quite yet.”

Ecommerce Payment vs. Traditional In-Store Processing

The biggest difference between selling online versus in a physical store comes down to one thing: physical presence.

In-store payments are “card-present” transactions where both the customer and their physical card are standing right in front of you. You can verify the card, watch them sign, or see them enter their PIN.

Online payments, however, are “card-not-present” (CNP) transactions, which fundamentally changes the risk profile. When someone orders from your online store at 2 AM, you never see their face or their actual card—and this invisible nature of ecommerce payment creates several key differences:

| In-Store Payments | Ecommerce Payments |

|---|---|

| Lower transaction fees (typically 1.5-2.5%) | Higher transaction fees (typically 2.9% + $0.30) |

| Lower fraud risk | Higher fraud risk |

| Immediate authorization | Authorization may include additional verification steps |

| Simpler PCI compliance | More complex PCI compliance requirements |

| Limited payment options | Multiple payment method options |

This higher risk is why online merchants typically pay more in processing fees and need stronger security measures.

Key Benefits of Modern Ecommerce Payment Systems

Today’s ecommerce payment systems offer advantages that would have seemed like science fiction just a decade ago.

The magic of one-click checkout has transformed the online shopping experience. By securely storing payment information through tokenization, returning customers can complete purchases with a single tap. One of our Memphis-based clients saw conversion rates jump 32% after implementing this feature—people simply buy more when it’s easier to pay.

Modern payment systems also break down global barriers with multi-currency support. Your little shop in Knoxville can now automatically display prices in euros, yen, or pounds, making international shoppers feel right at home. As one Tennessee artisan told us: “When we started showing prices in local currencies, our international sales jumped nearly 30% in the first month alone.”

Want to increase your average order value? Today’s payment technologies seamlessly integrate with buy-now-pay-later services and other financing options. This lets customers make larger purchases than they might otherwise consider. We’ve seen merchants boost their average order from $90 to $130+ simply by adding these flexible payment options.

Perhaps most exciting is the global reach now available to businesses of all sizes. The right payment system lets even the smallest Tennessee boutique sell to customers worldwide, accepting payment methods popular in different regions—from Alipay in China to iDEAL in the Netherlands.

Modern ecommerce payment systems don’t just process transactions—they open doors to new customers, new markets, and new growth opportunities for your business.

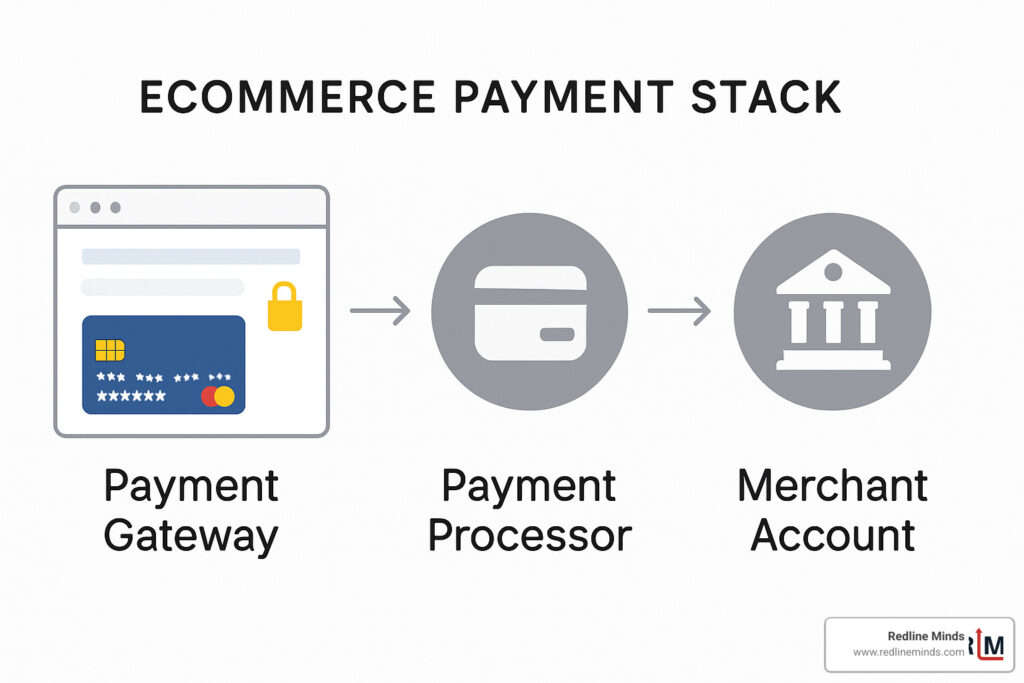

Core Components of an Ecommerce Payment Stack

To understand ecommerce payment processing fully, you need to know the three main components that work together to make online transactions possible:

Payment Gateways: Your Secure Checkout Front Door

Think of a payment gateway as the friendly but vigilant bouncer at your online store’s door. It’s the technology that securely collects and encrypts your customers’ payment information on your website – essentially the digital version of that card terminal you slide your card through at physical stores.

Your gateway performs several crucial jobs that keep transactions secure. It captures card details, wraps them in powerful encryption (turning “4111-2222-3333-4444” into something that looks like a cat walked across your keyboard), routes this protected information to your payment processor, and then relays the “approved” or “declined” message back to your eager customer.

You have two main gateway options to consider. Hosted gateways redirect shoppers to another site to complete payment (like when PayPal whisks customers away to their own checkout page). This approach is easier to set up and reduces your security burden, but creates a bit of a bumpy ride in the customer journey.

Embedded gateways keep customers snugly on your website throughout checkout. As one of our specialty retail clients in Nashville told us after making the switch: “Our cart abandonment rate dropped by 15% when we kept customers on our site for the entire checkout process.” The tradeoff? You’ll need more robust security measures on your end.

Payment Processors: The Money Movers

While your gateway is collecting information up front, your payment processor is working behind the scenes as the actual money mover. Think of processors as the financial dispatch center that coordinates with all the important players.

Your processor talks to card networks like Visa and Mastercard, communicates with your customer’s bank, gets authorization responses, and kicks off the settlement process that actually moves money into your account. They also batch transactions together (rather than processing each one individually) to make everything more efficient.

Payment processors must follow strict security guidelines outlined in the Payment Card Industry Data Security Standard (PCI DSS). These standards ensure that everyone handling credit card information maintains a secure environment – which is why you’ll typically pay a percentage of each transaction plus a fixed fee for their services. Those fees cover the cost of securely moving money, preventing fraud, and handling the risks that come with online transactions.

Merchant Accounts & Settlement Timing

Your merchant account is where the money lands after a successful transaction – it’s the specialized bank account that allows your business to accept and process electronic payments. Think of it as the final destination in the payment journey.

The flow of funds follows a predictable path: your customer’s payment gets authorized, the processor captures and temporarily holds those funds, then transfers them to your merchant account (minus their fees, of course). From there, you can move the money to your regular business bank account.

While authorization happens in seconds (that “approved” message your customer sees), actual settlement – the transfer of real money – typically takes 1-3 business days. Some providers offer faster settlement if you’re willing to pay a premium for speedier access to your cash.

One thing that sometimes surprises new online store owners is the concept of reserves. Payment processors may hold back a percentage of your transactions as a safety net to cover potential chargebacks (when customers dispute charges). This is especially common if you’re just starting out or if you sell in industries with higher dispute rates. As one of our furniture retail clients finded: “Understanding the reserve policy helped us better plan our cash flow during our first six months online.”

Understanding these three components—gateway, processor, and merchant account—gives you the foundation for making smart decisions about your ecommerce payment system that can directly impact your bottom line.

Behind-the-Scenes Transaction Flow

Now that we understand the components, let’s see how they work together in a typical ecommerce payment transaction:

Step-by-Step: From Click to Cash

Have you ever wondered what happens in those few seconds between clicking “Buy Now” and seeing your order confirmation? Let’s pull back the curtain on this digital magic trick.

1. Customer Initiates Payment

It all starts with a decision. Your customer has fallen in love with your products, steerd to checkout, and is now entering their payment information. This moment—fingers hovering over the keyboard, credit card in hand—is the culmination of all your marketing efforts.

2. Payment Gateway Encrypts the Data

As soon as your customer hits “Submit,” your payment gateway springs into action. It immediately takes that sensitive card data and transforms it into an unreadable code—like turning English into an alien language that only banks can understand. This encryption happens in milliseconds but provides crucial protection against digital eavesdroppers.

3. Payment Processor Authorizes the Transaction

The encrypted information now begins its journey through the financial system. Your payment processor acts like a traffic controller, routing the payment details to the right card network (Visa, Mastercard, etc.), which then connects with the customer’s bank. The bank performs a quick series of checks: Is this card valid? Are sufficient funds available? Does this purchase match the cardholder’s normal behavior?

“Most folks don’t realize their bank makes dozens of security decisions in less time than it takes to blink,” shared one of our Tennessee retail clients. “It’s pretty remarkable when you think about it.”

4. Gateway Confirms the Transaction Status

The bank’s decision—approve or decline—travels back through the same channels to your payment gateway. The gateway then translates this response into a customer-friendly message. For approved transactions, your customer sees that satisfying “Order Confirmed” screen. For declines, they receive guidance on what went wrong and how to fix it.

5. Funds Settlement to Merchant Account

While your customer is already dreaming about receiving their new purchase, the money isn’t quite in your account yet. At the end of the business day, your payment processor bundles all approved transactions into a batch and initiates the actual transfer of funds. This settlement process typically takes 1-3 business days before the money lands in your merchant account, ready for you to use in your business.

How Tokenization Powers Fast Repeat Purchases

Remember the last time you bought something online with just one click? That convenience is powered by a clever technology called tokenization—and it’s revolutionizing ecommerce payment systems.

Tokenization works like a coat check at a fancy restaurant. When a customer first shops with you, they “check” their real payment information and receive a token (a unique code) in return. For future purchases, they just need to present this token—not their actual card details.

This seemingly simple concept delivers powerful benefits for both you and your customers:

Your customers enjoy lightning-fast checkout experiences. No more fumbling for credit cards or typing long numbers—just click and buy. This speed is especially valuable on mobile devices, where typing can be cumbersome.

Your business benefits from improved security. Even if hackers somehow breach your system, they’d only find meaningless tokens, not actual card numbers. It’s like thieves breaking into a vault only to find worthless IOUs instead of cash.

Your conversion rates get a significant boost. One of our clients, a boutique home goods store, saw their repeat purchase rate jump by 38% after implementing tokenized payments. “Customers who used to abandon their carts are now completing purchases because it’s so easy,” the owner told us.

Tokenization also makes guest checkout less risky for shoppers. Many customers abandon carts when forced to create accounts, but with tokenization, you can offer the security of saved payment methods without requiring account creation.

The beauty of modern ecommerce payment systems is that all this complexity happens behind the scenes, creating what feels like magic to your customers—they click a button, and their purchase is complete. But understanding these mechanics helps you choose the right payment partners and optimize the experience for your unique business needs.

Choosing & Optimizing Your Ecommerce Payment Solution

Selecting the right ecommerce payment solution can make or break your online store. It’s like choosing the perfect engine for your car – get it right, and everything runs smoothly. Get it wrong, and you’ll face constant headaches.

Comparing Pricing Models & Fees

When it comes to payment processing costs, the details matter. Your choice directly impacts your profit margins, so understanding the fee structures is essential.

Flat-Rate Pricing keeps things beautifully simple. You pay the same percentage and fixed fee for every transaction, regardless of card type or volume. Think along the lines of 2.9% + $0.30 per transaction. This works wonderfully for smaller businesses who value predictability and straightforward accounting.

One of our bakery clients put it perfectly: “I don’t have time to analyze complex fee structures – I need to know exactly what each sale will cost me so I can price my products properly.”

Interchange-Plus Pricing offers a more transparent approach. You pay the actual interchange fee (set by card networks) plus a markup. For example: Interchange + 0.3% + $0.10 per transaction.

A furniture store owner we work with in Nashville switched to this model and told us, “Once our monthly sales hit $50,000, moving to interchange-plus saved us nearly $1,000 every month. It was like getting a free employee!”

| Pricing Model | Best For | Typical Structure |

|---|---|---|

| Flat-Rate | Small to medium businesses, predictable pricing | 2.9% + $0.30 per transaction |

| Interchange-Plus | Higher volume merchants, cost optimization | Interchange + 0.3% + $0.10 per transaction |

Don’t forget about those sneaky additional fees that can add up fast: monthly service fees, setup costs, chargeback penalties, international transaction surcharges, and currency conversion fees. Always read the fine print!

Payment Methods Shoppers Expect in 2024

Today’s shoppers want options – lots of them. The payment landscape has evolved dramatically, and meeting these expectations can significantly boost your conversion rates.

Credit and debit cards remain the foundation of ecommerce payment. They’re like the reliable minivan of payment methods – not the flashiest option, but trusted and used by almost everyone. Make sure you accept all major cards including Visa, Mastercard, American Express, and Find.

Digital wallets have surged in popularity, with Apple Pay, Google Pay, and PayPal leading the charge. According to recent research, 53% of online shoppers now reach for digital wallets before traditional payment methods. They love the speed and security these options provide.

“Adding Apple Pay was like flipping a switch on our mobile conversion rate,” shared a Nashville boutique owner we work with. “Suddenly customers weren’t abandoning their carts when faced with typing card details on their phones.”

Buy Now, Pay Later (BNPL) services like Affirm, Klarna, and Afterpay have revolutionized online purchasing. They allow customers to split payments into manageable installments, often without interest. Merchants offering BNPL options typically see their average order values jump by 20% or more – customers simply spend more when they can spread out payments.

Other options gaining traction include Pay-by-Bank direct transfers (great for larger purchases), mobile payments (essential as smartphone shopping continues to grow), and even cryptocurrency (appealing to tech-savvy customers and early adopters).

Security & Fraud Prevention Best Practices

With online transactions, security isn’t just important – it’s everything. Card-not-present transactions carry higher risk, making robust security measures essential for your ecommerce payment system.

![]()

The Address Verification System (AVS) acts as your first line of defense. It simply checks if the billing address entered matches what’s on file with the customer’s bank. A mismatch doesn’t automatically mean fraud, but it does raise a red flag worth investigating.

Requiring the Card Verification Value (CVV) – that little 3 or 4-digit code on the back of cards – adds another security layer. Since this code isn’t stored in the magnetic stripe or chip, requiring it helps verify that the customer actually has the physical card.

3D Secure Authentication takes things a step further. This additional verification (known as Verified by Visa, Mastercard SecureCode, etc.) adds an extra step where customers must verify their identity directly with their bank, usually through a one-time password sent to their phone.

Modern AI-Powered Fraud Detection systems act like digital security guards, constantly monitoring transactions for suspicious patterns. They can spot potential fraud in real-time based on hundreds of data points – far more effectively than manual reviews.

A local jewelry store we helped implement these measures shared a powerful result: “Our chargeback rate dropped from nearly 2% to just 0.4% after adding these security layers. That’s thousands of dollars saved, not to mention the stress reduction!”

Checkout UX Tips to Reduce Cart Abandonment

The final hurdle in your sales process – the checkout – is where too many sales go to die. Optimizing this critical touchpoint can dramatically increase your conversion rates.

Guest checkout options are non-negotiable in 2024. Forcing customers to create accounts before purchasing is the digital equivalent of making someone fill out a membership application before buying a sandwich – it’s unnecessary friction that drives people away. Studies show requiring account creation can increase abandonment by up to 23%.

One Tennessee-based outdoor gear retailer told us, “Adding guest checkout was like opening a floodgate of sales we didn’t know we were missing.”

Autofill functionality makes completing forms a breeze. When browsers can automatically populate shipping and payment details, checkout times plummet and completion rates soar.

The magic of a one-page checkout can’t be overstated. Each additional page in your checkout flow can reduce conversion rates by approximately 10%. Consolidating the process keeps customers focused on completing their purchase.

Clear progress indicators help customers see the light at the end of the tunnel. For multi-step checkouts, showing exactly where they are in the process reduces anxiety and abandonment.

Prominently displayed trust badges near payment forms reassure nervous shoppers. Security certifications, payment method logos, and money-back guarantees all signal that it’s safe to proceed.

Perhaps most critically, optimize your load speed. According to research, 53% of shoppers will abandon a site that takes longer than three seconds to load. This is especially true during checkout, where patience wears thinnest.

Mini-FAQ: Burning Questions on Ecommerce Payment

What is PCI compliance and do I need it?

PCI DSS (Payment Card Industry Data Security Standard) is essentially the rulebook for handling credit card data securely. And yes, if you accept credit cards, you need some level of compliance.

The good news? Your level of responsibility varies based on how you handle payments:

If you use a hosted payment gateway that redirects customers elsewhere for payment entry, your PCI burden is minimal – the provider handles most compliance requirements.

If you collect card details directly on your site, you’ll need to meet more stringent standards, including regular security assessments and maintaining a secure network.

Most payment providers shoulder much of this burden, but always clarify your specific responsibilities. As one client put it, “PCI compliance sounds scary until you realize your payment provider handles most of it for you.”

How do transaction fees really work?

Transaction fees typically have three components that work together:

- Interchange fees go to the customer’s issuing bank (typically the largest portion)

- Assessment fees go to the card network (Visa, Mastercard, etc.)

- Processor markup is what your payment processor charges for their service

For most online stores, these are bundled into a single rate (like 2.9% + $0.30). However, understanding this breakdown becomes valuable when negotiating rates as your volume grows.

Worth noting: premium rewards cards typically cost more to process than basic cards. That platinum card earning massive travel points? It likely costs you more to accept than a standard debit card.

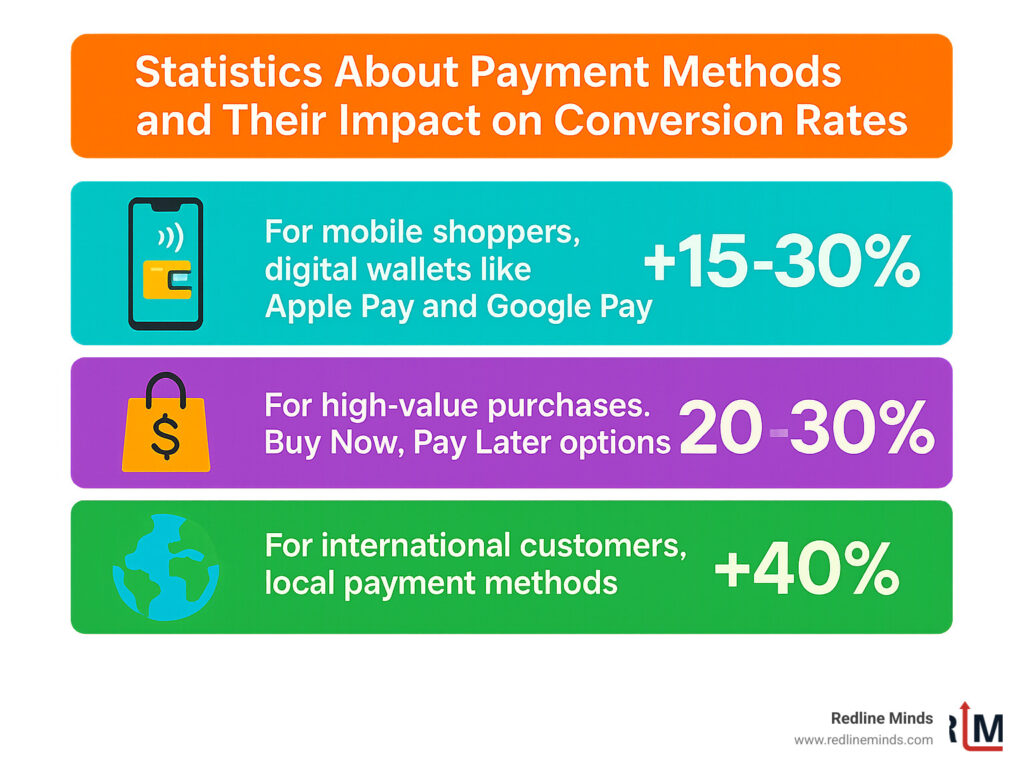

Which payment methods boost conversion the most?

The perfect payment mix varies by industry and audience, but some clear patterns emerge:

For mobile shoppers, digital wallets like Apple Pay and Google Pay can boost conversion by 15-30% by eliminating tedious form-filling on small screens.

For higher-value purchases above $100, offering Buy Now, Pay Later options can increase conversion rates by 20-30%, making larger purchases more accessible.

For international customers, offering local payment methods can improve conversion by 40% or more – shoppers strongly prefer familiar payment options.

The winning approach is analyzing your specific customer base and offering what they prefer. At Redline Minds, we help our clients find the perfect payment mix for their unique audience, leading to higher conversions and happier customers.

Conclusion

Understanding the mechanics of ecommerce payment processing isn’t just technical knowledge—it’s a strategic advantage for your online business. When you grasp how payments really work, you’re equipped to make decisions that directly impact your sales, customer happiness, and revenue.

Let’s take a moment to reflect on what we’ve covered:

The three pillars of any ecommerce payment system—payment gateways, processors, and merchant accounts—work together seamlessly to move money from your customer to your bank account. This invisible dance of data happens in seconds but involves multiple security checks that protect everyone involved.

Choosing the right payment solution is like picking the perfect pair of shoes—it needs to fit your unique business needs while providing comfort for your customers. The best solution balances reasonable fees with robust security, diverse payment options, and a smooth customer experience.

As one of our clients, a craft brewery in Nashville, told us: “Once I understood what was happening behind my checkout page, I could finally have meaningful conversations with payment providers instead of just nodding along.”

Your checkout experience directly impacts your bottom line. Small tweaks like offering guest checkout, showing clear progress indicators, and displaying trust badges can dramatically reduce cart abandonment. 53% of shoppers will leave a site that takes more than three seconds to load—speed matters, especially during checkout.

Security measures aren’t just about compliance—they’re about building trust. Features like tokenization, 3D Secure verification, and fraud detection tools create a protective shield around both your business and your customers.

At Redline Minds, we specialize in helping Tennessee businesses and beyond implement payment systems that maximize conversion while minimizing costs and security risks. We understand that every online store is unique, with different products, customers, and growth goals.

Ready to level up your ecommerce payment system? Here’s your action plan:

- Shop your own store—experience the checkout process exactly as your customers do

- Take a hard look at your processing fees compared to industry standards

- Make sure you’re offering the payment methods your specific customers prefer

- Review your security measures against current best practices

The payment process isn’t just the final step in a transaction—it’s often the difference between a completed sale and an abandoned cart. Invest in getting it right, and you’ll see the results in higher conversion rates and happier, returning customers.

For more detailed information about specific payment options for your ecommerce store, check out our guide on Ecommerce Payment Options.