Splitting Bills and Thrills with Buy Now Pay Later Solutions

The Rise of Flexible Payments: Why BNPL Is Reshaping Online Retail

The best buy now pay later solutions for online retailers in 2026 include:

| Provider | Best For | Key Feature |

|---|---|---|

| Affirm | High-value purchases | Long-term financing, no late fees |

| Afterpay | Fashion & lifestyle retail | Pay-in-4, capped late fees |

| Klarna | Broad retail use | Multiple payment options |

| PayPal Pay Later | Existing PayPal merchants | Built into PayPal ecosystem |

| Shop Pay Installments | Shopify stores | Native integration, boosts AOV |

Something shifted in how people pay online — and it happened fast.

Buy now pay later solutions have gone from a niche checkout option to a mainstream payment method that customers actively look for before completing a purchase. In fact, more than half of US customers have already used a BNPL service — and that number keeps climbing.

For mid-sized online retailers, this isn’t just a trend to watch. It’s a revenue opportunity sitting right at your checkout button.

BNPL works simply: a customer splits their purchase into smaller installments — often interest-free — spread over weeks or months. They get the product now. You get paid in full upfront. The BNPL provider takes on the repayment risk.

That last part matters a lot for your business.

The appeal for shoppers is obvious — smaller payments feel more manageable than one large charge. But the appeal for merchants is just as strong. More completed purchases. Higher average order values. And access to younger buyers who prefer installment payments over traditional credit cards.

This guide breaks down the top BNPL providers, what to look for when choosing one, and how to integrate it into your store the right way.

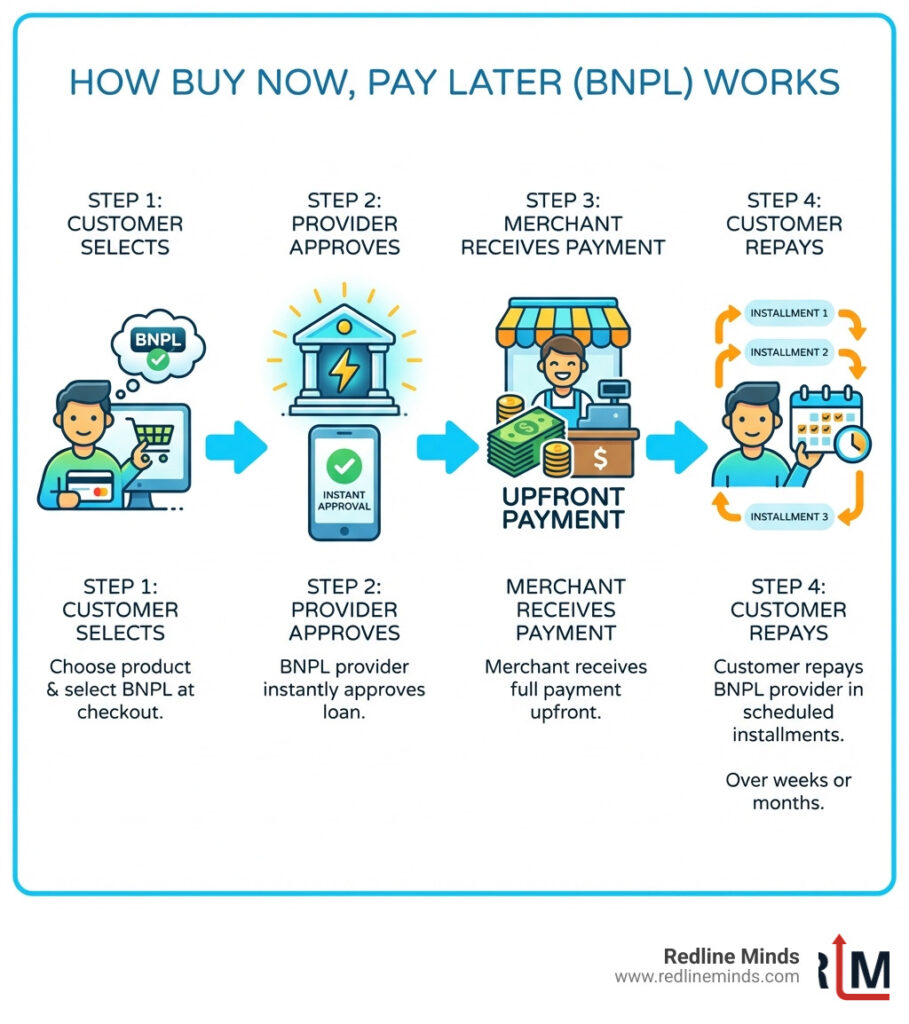

How BNPL Works: A Look Behind the Checkout Button

To understand why buy now pay later solutions are taking over, we need to peek under the hood of the checkout process. From the outside, it looks like a simple “split payment” button. Behind the scenes, it’s a sophisticated financial handshake between the consumer, the merchant, and the BNPL provider.

For the consumer, the process is incredibly streamlined. When they reach your checkout page, they select their preferred BNPL provider. Instead of filling out a lengthy credit application, they usually enter a few basic details. The provider performs a lightning-fast “soft” credit check and offers an instant approval decision. If approved, the customer pays a small down payment (usually 25%), and the transaction is complete.

For us as merchants, the process is even better. Once the customer clicks “buy,” the BNPL provider pays us the full amount of the purchase immediately (minus a transaction fee). We don’t have to wait for the customer to finish their installments to get our cash. Most importantly, the provider assumes all the risk. If the customer misses a payment later on, that’s between them and the provider. Our revenue is already secure in our bank account.

How Providers Make Money

You might wonder, “If it’s interest-free for the customer, how do these companies stay in business?” It’s a fair question. BNPL providers primarily make money through merchant fees. They charge retailers a percentage of each transaction, which is often slightly higher than standard credit card processing fees. However, most retailers find this a worthwhile trade-off for the increased sales volume.

Additionally, providers may earn revenue through:

- Consumer Late Fees: If a shopper misses a scheduled payment.

- Interest: While the “Pay-in-4” model is usually interest-free, longer-term plans (like 12 to 36 months) often carry an Annual Percentage Rate (APR).

- Service Fees: Some models include small administrative fees charged at the time of purchase.

Benefits for Shoppers and Merchants

The reason buy now pay later solutions have exploded in popularity is that they solve problems for both sides of the transaction.

For shoppers, BNPL increases purchasing power without the “debt trap” feel of a high-interest credit card. It’s a budgeting tool that allows them to manage cash flow. According to research, 15% of Americans don’t use credit cards at all anymore, largely due to high interest rates. BNPL fills that gap.

For merchants, the benefits are quantifiable:

- Higher Conversion Rates: Customers are less likely to abandon their carts when the total price is broken down into “bite-sized” chunks.

- Increased Average Order Value (AOV): When a $200 purchase becomes four $50 payments, customers are often more willing to add an extra item to their cart. In fact, merchants using Shop Pay Installments experience up to a 50% increase in average order value.

- Attracting Younger Demographics: Millennials and Gen Z are the driving force behind this trend. Data shows more than 26% of millennials and almost 11% of Generation Z shoppers used BNPL for their most recent purchases.

Understanding the Risks of Buy Now Pay Later Solutions

While the “thrills” of easy shopping are great, we have to be honest about the risks. For consumers, the biggest danger is overspending. It is easy to lose track of multiple $20 payments across different providers, leading to a “death by a thousand cuts” for their monthly budget.

From a merchant’s perspective, returns can become a bit more complicated. Since the customer is paying a third party, the refund process involves coordinating between your store and the BNPL provider to ensure the customer’s loan is canceled or adjusted. The Department of Financial Protection and Innovation offers tips for handling returns to help consumers and businesses navigate these tricky waters.

Furthermore, BNPL services generally offer fewer consumer protections than traditional credit cards. If there is a dispute over a damaged item, the legal framework for BNPL is still evolving, leaving shoppers in a grey area.

Exploring the Top Buy Now Pay Later Solutions for Your Business

Choosing the right provider is about more than just picking a name you recognize. Different buy now pay later solutions cater to different types of products and customer behaviors. Some focus on small, frequent purchases (like clothing), while others are built for big-ticket items (like furniture or electronics).

Popular BNPL Providers and Their Features

Affirm Affirm is a heavy hitter in the US market, known for its transparency and flexibility. They offer a range of plans, from the standard interest-free “Pay-in-4” to longer-term installments lasting up to 36 months. One of their biggest selling points for consumers is that they never charge late fees—ever. For merchants, Affirm’s “Adaptive Checkout” dynamically shows the most relevant payment options to each customer based on their cart size and credit profile.

Afterpay If you are in the fashion, beauty, or lifestyle space, Afterpay is likely already on your radar. They pioneered the “Pay-in-4” model, where the customer pays over six weeks. Afterpay is incredibly popular with younger shoppers, and their app acts as a shopping directory, sending high-intent traffic directly to your store. They do charge late fees, but these are capped to prevent debt from spiraling.

Klarna Klarna positions itself as an all-in-one shopping ecosystem. They offer “Pay in 4,” “Pay in 30 days,” and traditional financing for up to 36 months. Klarna is famous for its smooth user interface and its “Purchase Power” metric, which gives users a clear idea of how much they can spend responsibly. With over 150 million shoppers globally, they bring a massive existing user base to any merchant who integrates them.

PayPal Pay Later For many of us, PayPal is already a core part of our payment stack. PayPal Pay Later allows you to leverage that existing trust. They offer “Pay in 4” for smaller purchases and “PayPal Monthly” for larger ones. Because so many customers already have a PayPal account with their shipping and billing info saved, the friction to use their BNPL option is almost zero.

Shop Pay Installments For retailers running on Shopify, Shop Pay Installments is often the path of least resistance. It’s built directly into the Shop Pay checkout, which is already one of the fastest converting checkouts on the web. It offers the same bi-weekly and monthly options as Affirm (who powers the service), but with the added benefit of being natively integrated into your Shopify admin for easy reporting.

Integrating BNPL: A Strategic Move for Ecommerce Growth

Integrating buy now pay later solutions isn’t just a technical task; it’s a strategic decision. We’ve seen how the right payment mix can transform a struggling store into a high-growth engine. But before you flip the switch, you need to evaluate which provider aligns with your business goals.

Key Factors in Choosing Buy Now Pay Later Solutions

| Factor | What to Look For |

|---|---|

| Transaction Fees | Typically range from 2% to 8%. Balance this against your margins. |

| Integration | Does it work with your current platform (Shopify, BigCommerce, etc.)? |

| Disbursement | How fast do you get your money? (Usually 1–3 business days). |

| Customer Base | Does the provider’s audience match your target demographic? |

| Credit Limits | Are the limits high enough for your most expensive products? |

The regulatory side is also worth noting. The Federal Reserve Bank of Kansas City discusses bank and payment network perspectives regarding the rise of these services, noting that while they offer great utility, they are coming under increased scrutiny from financial regulators. Choosing a provider with a strong reputation for compliance is vital for long-term stability.

How to Effectively Promote BNPL to Your Customers

Simply adding the button at checkout isn’t enough. To see a real boost in AOV and conversion, you need to promote these options throughout the buyer’s journey.

- Announcement Banners: Place a banner at the top of your homepage letting customers know they can pay in installments.

- Product Page Messaging: This is the most effective tactic. Show the “as low as $X/month” price right next to the full price. This makes high-ticket items feel immediately affordable.

- Email Marketing: Include the BNPL logo in your abandoned cart emails. Sometimes the only thing standing between a customer and a purchase is the immediate “sticker shock.”

- Marketing Toolkits: Most providers offer resources to help you. For example, Shopify provides a marketing toolkit with compliance guidelines and approved messaging to ensure you’re advertising the service legally and effectively.

The Fine Print: Credit Scores, Regulation, and Responsible Use

One of the most common questions we hear is: “Will this hurt my customer’s credit score?”

Generally, the answer is no—at least not initially. Most buy now pay later solutions perform a “soft” credit check, which does not impact a credit score. However, things are changing. Some providers have started reporting payment history to credit bureaus. This means on-time payments could actually help a customer build credit, but late payments will definitely hurt it. The CFPB explains how BNPL can impact credit scores in detail, noting that the impact varies by provider.

The industry is also seeing a shift in regulation. In the past, BNPL was often called the “Wild West” of finance because it lacked the strict oversight of credit cards. However, the Consumer Financial Protection Bureau (CFPB) is now taking a much closer look at these companies to ensure they treat consumers fairly and don’t encourage “debt stacking.”

How to Use BNPL Responsibly and Avoid Debt

As responsible retailers, we want our customers to be happy with their purchases, not stressed by them. Encouraging responsible use is good for business—it leads to lower return rates and higher customer lifetime value.

We recommend that shoppers:

- Set a Budget: Don’t treat BNPL as “free money.”

- Track Payments: Use the provider’s app to keep an eye on due dates.

- Auto-Pay: Set up automatic payments to avoid late fees.

- Needs vs. Wants: Use BNPL for essential large purchases or well-planned treats, rather than impulsive daily spending.

Frequently Asked Questions about BNPL

What happens if I miss a BNPL payment?

Missing a payment can lead to several consequences. Most providers will charge a late fee, which can range from a few dollars to a percentage of the order. Beyond the cost, your account will likely be suspended, preventing you from making new purchases. Perhaps most importantly, some providers report late payments to credit bureaus, which can damage your credit score.

Are buy now, pay later plans safe to use?

Yes, they are generally very safe. Providers use high-level encryption to protect your data, and because you aren’t sharing your full credit card details with every merchant, it can even be more secure in some cases. However, the “risk” is often more financial than technical. The Office of the Comptroller of the Currency outlines risk management for BNPL programs, emphasizing that consumers should be aware of the potential for over-borrowing and the limited dispute protections compared to traditional banking.

What are the main alternatives to BNPL?

If BNPL isn’t the right fit, there are other ways to manage large purchases:

- Traditional Credit Cards: These offer better dispute protection and rewards, but often carry much higher interest rates.

- Personal Loans: Better for very large, long-term expenses (like home renovations).

- Layaway: The “old school” version of BNPL where you pay installments but don’t get the item until it’s fully paid off.

- Saving: The most “responsible” but least instant option!

Conclusion: Is BNPL the Future of Payments?

The data is clear: buy now pay later solutions aren’t going anywhere. They have become a fundamental expectation for the modern shopper. For us as retailers, they offer a powerful way to reduce friction, increase sales, and build loyalty with a new generation of consumers.

However, success isn’t just about adding a button. It’s about choosing the right partner, integrating it seamlessly into your user experience, and promoting it responsibly. As the industry matures and regulations tighten, the winners will be the merchants who use these tools to genuinely help their customers afford the things they love.

Whether you’re selling sustainable activewear or high-end electronics, flexible payments are the key to unlocking the next level of your store’s growth. For expert guidance on integrating the right payment systems for your store, Redline Minds can help you steer your ecommerce payment options toward a more profitable future. We specialize in helping mid-sized and B2B stores navigate these complex choices so you can focus on what you do best—running your business.

Share this article

Tap into years of experience and turn your site’s visitors into buyers.

Related Posts

-

The Definitive Guide to Virtual Ecommerce Directors

Hire a virtual ecommerce director to scale revenue, optimize CRO, and lead remote eCommerce growth strategically.

-

The Best SEO Tool for Shopify Stores

Discover the best SEO tool for Shopify in 2025. Compare top apps like TinyIMG & Booster SEO for…

-

How to Audit Your Store Before Google Does

Conduct your ecommerce site audit: fix revenue leaks, boost conversions, and optimize performance with our expert checklist and…